Yesterday I did a piece analysing the potential for the CHF/EUR currency pair to be used as an inflation hedge. The results were pretty good. However, I noted that recent CHF/EUR moves seem to have been underexagerrated relative to inflation.

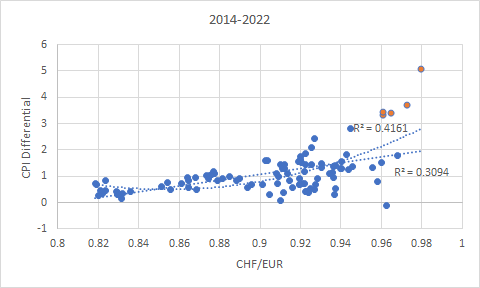

Here is the chart I showed to highlight that:

The reader will see the last five months highlighted in orange. They are clearly pretty far off the linear regression line. I interpreted this to mean that markets have been hesitant to classify the present inflation as sticky so they have not priced the CHF/EUR currency pair for present rates of inflation. Hence, ‘inflation hesitancy’.

If this is true — this is an interpretation on my part and may be wrong — but if it is true, then CHF/EUR has underperformed relative to what it should have. And this underperformance may be corrected if markets decide that the inflation is here to stay.

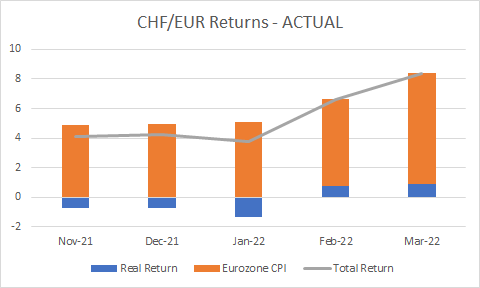

Here’s a thought experiement: what would returns for the CHF/EUR have looked like relative to inflation if there were no inflation hesitancy? Below we compare a model that tries to capture that with the actual returns we have seen.

What this tells us is that if CHF/EUR hwere behaving normally relative to the current inflationary dynamics, we would have seen absolutely incredible returns these past five months. Not only would it have maintained oyur wealth, but it would have given us a monthly real return of anywhere from 3% to 7%.

Okay, but this is a fairy tale. It didn’t happen. So what are we to make of this exercise? Consider it a bull-case for CHF/EUR moving forward if I am right about inflation hesitancy and the market changes its mind on the stickiness of inflation.