How has the present inflation impacted factors?

And how does this stack up relative to history?

I have just republished two posts from my old blog here that I wrote in September. I am republishing them (a) on the assumption that many subscribers have not seen them and (b) because I want to follow up on the work done in them today.

In those posts I looked at how various factors performed during previous inflations. Specifically, I tested value, size, momentum and two quality factors (profitability and investment). The results were complex and I would encourage you to read those posts if you are interested, but I found that factor investing for the most part allowed investors to make excess gains during periods of inflation.

Well, we are now nearly a year in on the present inflation. Since March 2021, the average CPI rate in the US has been 5.5%. I think that this period can safely be called a year of inflation. So, let’s check back in on our factors. (Here I use the excess returns on a given factor relative to its history — so, a reading of 1.1 indicates a 10% higher alpha and so on).

Now this is interesting. Over the past year, value and quality have outperformed. Value has always outperformed in inflationary periods, but the last year’s outperformance has been one for the record books. Momentum has not done well and size has gotten absolutely crushed. This is surpising as size and momentum had fairly reliable outperformances during inflations historically.

But when it comes to quality the world has been turned upside down. Investment has historically outperformed, but not by the amount that is has in the past year. Meanwhile, profitability’s outperformance has been phenomenal. Yet profitability was the one metric that performed poorly historically during inflations.

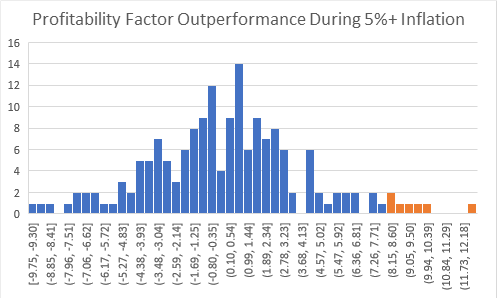

To get a sense of how unusual this is take a look at this histogram which shows the alpha of the profitability factor when inflation is above 5%.

Six of the past twelve months fall into the area highlighted in orange. In fact, only one other month in history falls into this area of the graph (June 1969).

If the past year is anything to go by, inflation has more than a few tricks up its sleeve. Some of the factors have worked to outpace the recent inflation, but some that have been reliable in the past have failed. In addition to that, some that were absolute duds in the past have been reshuffled to the top of the deck.

What lesson would I take from this? First of all, that all inflations are unique. And secondly, that we cannot rely completely on historical patterns in data. These patterns are useful and should be understood, but they have to be handled with care and applied to actual investment decisions prudently.