Is this or is this not a recession?

It doesn't matter, there are much bigger changes afoot

The GDP report for the US is out. As everyone surely knows at this stage, it showed that the economy contracted for the second quarter in a row — which is one popular indication that the economy is in recession. The economists are now becoming obessesed with this definition as we see that, despite persistant negative growth, we do not see other recessionary indicators such as rising unemployment.

Frankly, the debate is pointless and misleading. Is the US economy in a recession? On the basis of negative real income growth it certainly is. On the basis of labour market growth it is not. What economists are learning is the hard truth that just because everyone has jobs, they can nevertheless become poorer. If I flew to Somalia as an economic advisor and told them they could solves their 20% unemployment rate by printing money and giving everyone a job I would not be lying. But as the economy collapsed in an inflationary heap and everyone got much poorer, the Somalians would realise that I had commited a rather grevous sin of ommision.

A few notes on the actual numbers — and the arguments from the US bulls related to them — before moving on to the general picture and meaning of these numbers.

Some economists are saying that the negative growth is due to a quirk in inventory accumulation growth. Inventory accumulation growth contributed just over -2% to overall GDP growth and is a measure with high and largely random variability. Between Q3 2018 and Q2 2022 inventory accumulation growth had a standard deviation of 20.3. But what these economists do not mention is that net export growth contributed a large +1.4% to real GDP growth in Q2. Net export growth is just as highly variable as inventory accumulation growth, with a standard deviation in this time period of 22.7. So, the two ‘random’ events cancel each other out.

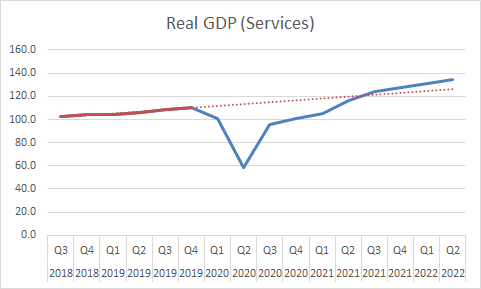

What we can draw from this is that, with the random variables put to one side, the rest of the real GDP picture is grim. The main problems are consumption of goods and domestic investment. Some economists are saying that the falling goods consumption is due to consumers switching back to services consumption from goods consumption after the pandemic. But this does not fit the data. If you project the pre-pandemic trend forward, you see that consumers started consuming services at their trend levels by Q2 2021. Since then, consumption of services has risen above pre-pandemic trends.

So, why the fall in goods consumption? The answer is simple enough: inflation is making people poorer. You can see this if you compare nominal and real spending on goods consumption. On a nominal basis in Q2 2020 goods consumption rose 6% from the previous year. Yet on a real basis it fell -3.2% in the same time period. People are spending their higher nominal income and they are getting less stuff for it. Those of us who set monthly budgets are all aware that this is happening. Either we are restricting consumption or we are finding that our old monthly budgets fall short of the new prices.

What about investment? The biggest driver is investment in structures. Non-residential structures contributed -0.72% to real GDP, while residential structures contributed -0.71%. When we look at nominal and real metrics we see the same dynamics as with consumption. In Q2 2022 annual nominal growth in structures investment was +9.8% and +8.9% in non-residential and residential respectively. But real growth in the same period was -6.4% and -5% respectively. People are investing more of their growing nominal incomes in structures, but they are getting less bricks and mortar for their money.

Overall then, we are seeing an obvious inflationary recession where people remain employed, but grow poorer and poorer over time. Everyone is experiencing this personally and it is bizarre that the economists are not talking about it. They seem completely out of touch both with peoples’ experiences and with the actual data, focused instead on their own meaningless ‘definitions’ that are arbitrary and made up.

What is going on? Simply put, the West is getting poorer. We are seeing two things at once. First of all, policymakers have lost the plot and started intervening heavily into the economy with lockdowns and various other policies that destroy the supply-side of the economy. Secondly, we are seeing an enormous geopolitical shift centered around the war in Ukraine. The old model where the rich West runs large trade deficits with the poorer developing countries in exchange for worthless paper is coming to an end. We are exacerbating this transition by engaging in self-destructive sanctions policies that interfere with markets in everything from energy to fertiliser.

In a few words: the West is in decline and our leaders are greatly accelerating and exacerbating this decline. They can cover this up with redundant arguments about what is and isn’t a recession for so long. But at some point either the inflation will get worse — perhaps by gas shortages in Europe this winter — and/or the unmeployment rate will spike. At that point, the underlying dynamics will become too obvious to ignore. For politicians and the general public anyway. Economists will likely find some other redundant nuance to debate and distract.

@philippilk

8/ The Russians win either way. Either we break the sanctions or our economies collapse and our societies collapse into chaos. Win-win for Putin. So we may as well give the Russians the win that doesn’t absolutely destroy us.

5:49 PM · Aug 27, 2022

Can't wait for the 2022/23 Winter to arrive.

I been talking about the hidden decline for 10+ years. I have been amazed that it has taken this long to pan out - we are only at the beginning of this process (it is not an event). This process will extend for as long as it takes to balance the energy system with the financialised one.

https://austrianpeter.substack.com/p/the-financial-jigsaw-part-2-the-end?s=w