PPP Now Determines RMB-USD

And if this trend holds it could threaten the USD's reserve currency status

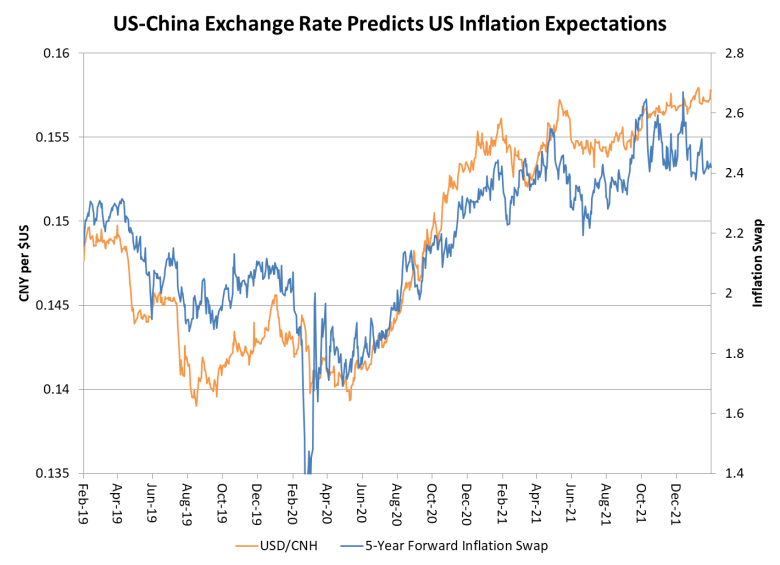

David Goldman has written a very interesting article for the Asia Times about the correlation between the RMB-USD exchange rate and inflation expectations. Here is his key chart:

And here is his conclusion:

Remarkably, the best predictor of US inflation expectations during the past three years is the RMB’s exchange rate against the US dollar. That’s because the marginal item bought by an American consumer with the $6 trillion of pandemic stimulus handouts is likely to be imported, and likely to be imported from China. China’s exchange rate affects the prices of so much of America’s goods consumption that the RMB moves inflation expectations in the US.

Hats off to Goldman for finding the correlation. I wouldn’t have known about it were it not for him. But I think the inference he draws from it is wrong.

The more conventional interpretation of this correlation is that the Purchasing Power Parity (PPP) relationship now holds between China and the US. That is, Goldman has the causality backwards. Under PPP when rices rise faster in one country than in another, the exchange rate adjusts so the prices remain the same — adjusted by the exchange rate — in both countries.

Why is this also impacting inflation expectations? Because inflation expectations are just lagged inflation.

But here’s the thing. This relationship is a recent one. Here are US-China inflation differentials plotted against the RMB-USD.

It appears that the PPP relationship did not hold until roughly 2018. We can see this more clearly by running two regressions, one on data pre-2018 and one on data post-2018.

Yup, there you have it: PPP started holding for this currency pair around 2018.

This is bad news for the US. If you think, as I do, that there is a good chance that inflation will be a problem for the US (and probably the whole West) for the next decade, then the PPP relationship between the RMB-USD could cause a decline in the stature of the USD.

Why? Because if inflation continues apace in the US and remains subdued in China, the RMB will appreciate continuosly against the USD. This will make the RMB ever more attractive to those who want a ‘safe’ currency. Effectively, the US could ‘inflate away’ the USD’s status as the world’s reserve currency.

Even a more optimistic assessment is bad news for the US. At the very least, this dynamic will likely make the RMB ever more attractive as an alternative reserve currency — and this will compete with the USD on the world stage.

There has been a lot of saber-rattling about China in the US in recent years. Maybe the US should be more focued on getting their own house in order rather than beefing up its military posture against China. But what do I know? I’m just an economist.