The consequences of inflation and rate hikes

Central banks are stuck between a rock and a hard place, but its time for them to come clean about the situation

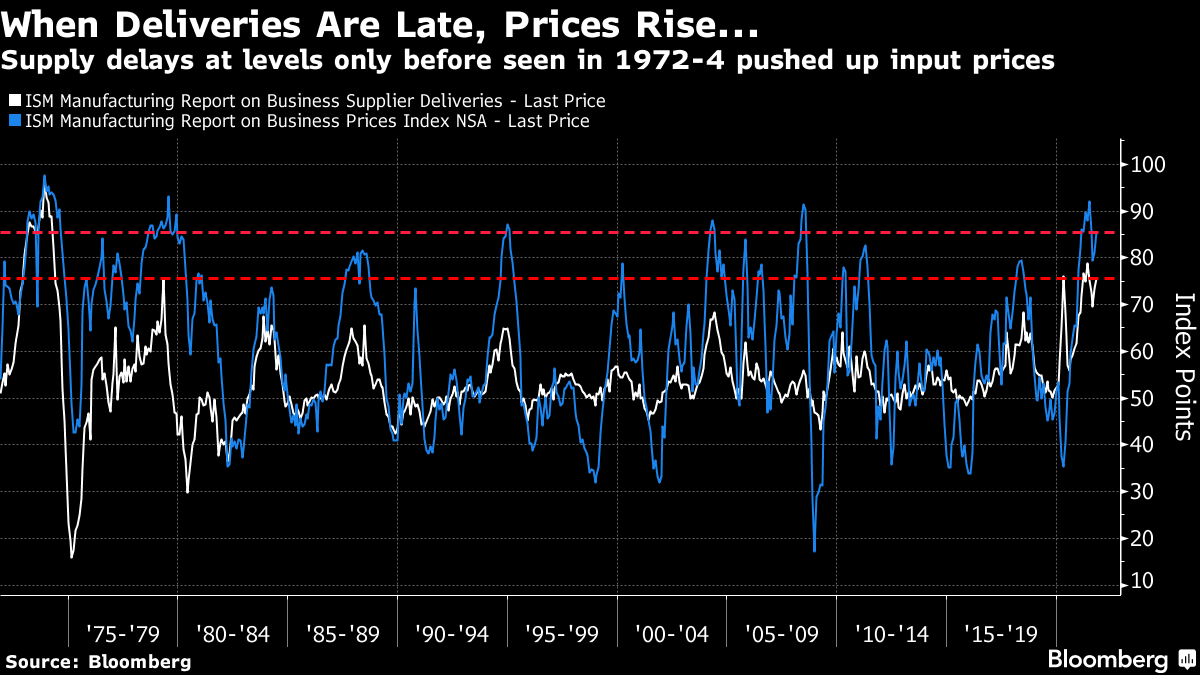

At this point it is obvious that the inflation that we are experiencing is probably not transitory. It is also increasingly obvious that this inflation is being driven by problems in supply chains — at both a global and a local level.

The following chart shows manufacturing deliveries in the United States together with the price of the goods being supplied. As we can see, we are now back to the 1970s in terms of supply chain disruptions.

Markets are starting to digest this too. Since they now seem unconvinced by the ‘transitory inflation’ narratives, they are starting to consider the prospect of interest rate hikes on the part of central banks.

The following chart shows Fed Funds Futures Forward curves. The coloured lines are basically market expectations of Federal Reserve interest rates hikes. Note that every few days the market pulls the curve leftwards — this signifies that the market expects the interest rate hikes to occur sooner rather than later.

Interestingly, however, some central banks — or at least, the Bank of England — has noted that interest rates are unlikely to solve supply chain problems. (They must be reading the pieces I’ve been publishing at Unherd!). Consider the following section of a speech given by Monetary Policy Committee member Silvana Tenreyro:

a range of temporary factors have been pushing CPI inflation above target, and will continue to do so over the coming months. Some of these, such as base effects and the direct impact of energy price rises, are short-lived, and monetary policy can do little to offset them: much of the effect of policy would not come until after their impact had faded; more important will be any indirect effects of energy prices on real incomes or production costs. The effects of supply chain disruption should also be temporary, and unwind as supply of some goods increases, and as demand rotates back towards pre-Covid consumption patterns.

There is probably a lot of truth in this. Monetary policy shocks can create a recession and thereby curb demand for goods and services, but it is not clear that they can fix supply chain shortages. A rate hike and recession may ease pressure on these supply chains sufficiently to allow producers more breathing room to fix the problem — but it may not. The effects are highly uncertain and not studied at all.

Tenreyro is onto something. But she is two polite to note two things — both of which are of enormous importance.

First of all, it is becoming increasingly clear that supply chain disruptions are the belated effects of the lockdowns and vaccine mandates on the economy. These may get worse in the future, not better. Last week New York activated its mandate — and almost 1 in 10 city workers simply walked out of their jobs. That is a lot of disruption and given that public employees skew left politically, private sector walkouts are likely to be even higher if mandates are enforced. Companies in the US are already talking about pulling government contracts that come with vaccine mandate clauses attached.

Secondly, Western economies are currently very fragile to a rate hike. We have not seen a significant financial market or economic downturn since 2008. This has been a long economic cycle. And with rock bottom interest rates, a lot of fragilities have built up. Corporate borrowing has gone gangbusters — and recently companies have shown some signs of becoming addicted to very low quality borrowing. Housing markets look extremely hot too, with valuations matching their 2008 highs in many markets. Finally, stock markets are currently more overvalued than they have been at any time except during the Dotcom bubble of the late-1990s.

These fragilities are a direct outcome of the low interest rate policies of central banks across the world. So, these central banks have boxed themselves in somewhat. If they fail to raise interest rates, they will likely take the blame — fairly or unfairly — if inflation spirals out of control. But if they do raise rates, all the crazy behaviour that the low rates have been encouraging in financial markets will unwind quickly and we may face a financial crisis as bad or worse than we did in 2008.

Now imagine the absolute worst case scenario: the central banks raise interest rates, financial and housing markets collapse, the economy slips into recession and the inflation does not abate because the interest rate hike fails to solve the supply chain problems created by lockdowns and vaccine mandates. We would then get stagflation on steroids; the 1970s meets the Great Recession of 2008-09.

Consider all of this and you have to sympathise with those running our central banks right now. The only message I would give them is this: get real about the source of this inflation and be honest with people that the public health measures enacted in the past two years could be having catastrophically bad economic consequences.