Australia's Magical Balance of Payments

Foreign capital flows run the show in Oz - but for how long?

When we glance at Australia’s macroeconomic statistics, what immediately stands out at us is that the country has been effectively running a fairly large and consistent current account deficit since statistics started to be collected.

Now, Australia is by no means a developing country. But nor is it a global hegemon, like the United States. This leads us to wonder why the Aussies have been ‘getting away with’ such large and consistent current account deficits.

The reason is that the imbalance is not really due to trade, unlike in the United States. Australians pretty much sell as much goods and services as they buy from abroad. Rather it is the ‘income balance’ in the current account that leads to the persistant deficits.

The ‘income balance’ on the current account is basically the amount of money that Australia is paying out to the rest of the world in rents. The extremely negative income balance — which has gotten much more negative since the early-1990s — is a reflection of the fact that a lot of Australian capital is owned by foreigners.

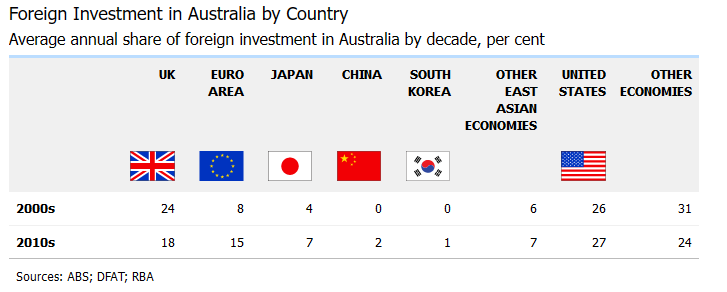

Who owns it? Relative to their size, it is mostly owned by the British.

Yes, the Americans have been playing catch up in recent years. But surprisingly large amounts of Australia are still owned by, well, by the mothership. (Pay attention Australian republicans!).

Basically, for most of history, most of Australia’s main companies were listed on the London stock exchange and bought by the British. This is changing, however, with Australia’s largest mining company (and the FTSE’s largest stock) announcing this year that they will exit the London stock exchange in favour of the domestic. Many others have focused on getting their listings on the New York exchanges.

But it would be misleading to think that equities drive the show. In fact, foreigners own large amounts of Australia mainly through the debt markets.

What have these foreigners being buying? Until 2008, the answer was: banks and other corporates. After 2008, the answer has been: public debt, mining and other corporates.

What does all this mean? In order to understand, we must turn to one more datapoint; namely, the currency in which the ownership of Australian assets is in.

What this chart shows is that Australians hold plenty of foreign assets. They are, in a sense, well-diversified. But foreigners are not very well-diversified in Australia. They are basically long the Australian dollar — and heavily so.

Recall that in the last piece we started by investigating the drivers of the Australian dollar. Now you can see why. If the dollar starts to lose value due to global inflation, those assets held by foreigners are going to look less and less attractive.

Even before the recent turmoil, there have been signs of instability — which worsened drastically during the crisis of 2020. Here is a chart that shows changes in the Net International Investment Position (NIIP) of Australia. The NIIP is effectively the amount of assets that foreigners own. These components show what is driving these changes.

Even eyeballing this chart we can see some of the instability in certain components over the past decade or so. For one, transactions have fallen — meaning that foreigners are buying less. Since 2020, this has been due to a massive contraction in the current account deficit due to a fall in imprts during the recession. But the trend is visible prior to that.

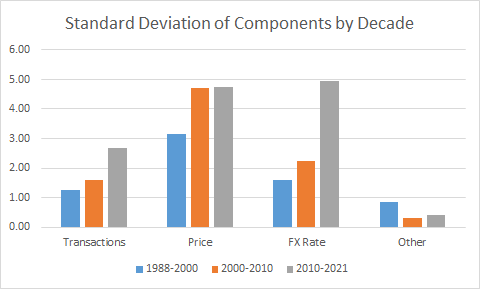

More interestingly is the volatility. Here are the standard deviations of each component by decade.

The exchange rate has become far more volatile in the last decade, as we can see. This represents a ‘risk’ for investors and could well explain in part why transactions have fallen. Note that these transactions too have become more volatile.

I believe what this data is showing is what is colloquially known in markets as Australia being a ‘risk-on trade’. Investors buy Australia when they’re feeling upbeat and confident. They sell when confidence wanes. This generates instability and volatility.

Now consider what might happen if global inflation puts structural pressure on the Australian dollar. Investors will then be looking at an asset that has more that could go wrong with it, at the same time as the currency it is denominated in becomes less stable. Of course, the underlying companies — many of them, anyway — will still be fine. The mines will still supply iron ore to the Chinese. But the assets that represent the companies could end up looking less attractive regardless.